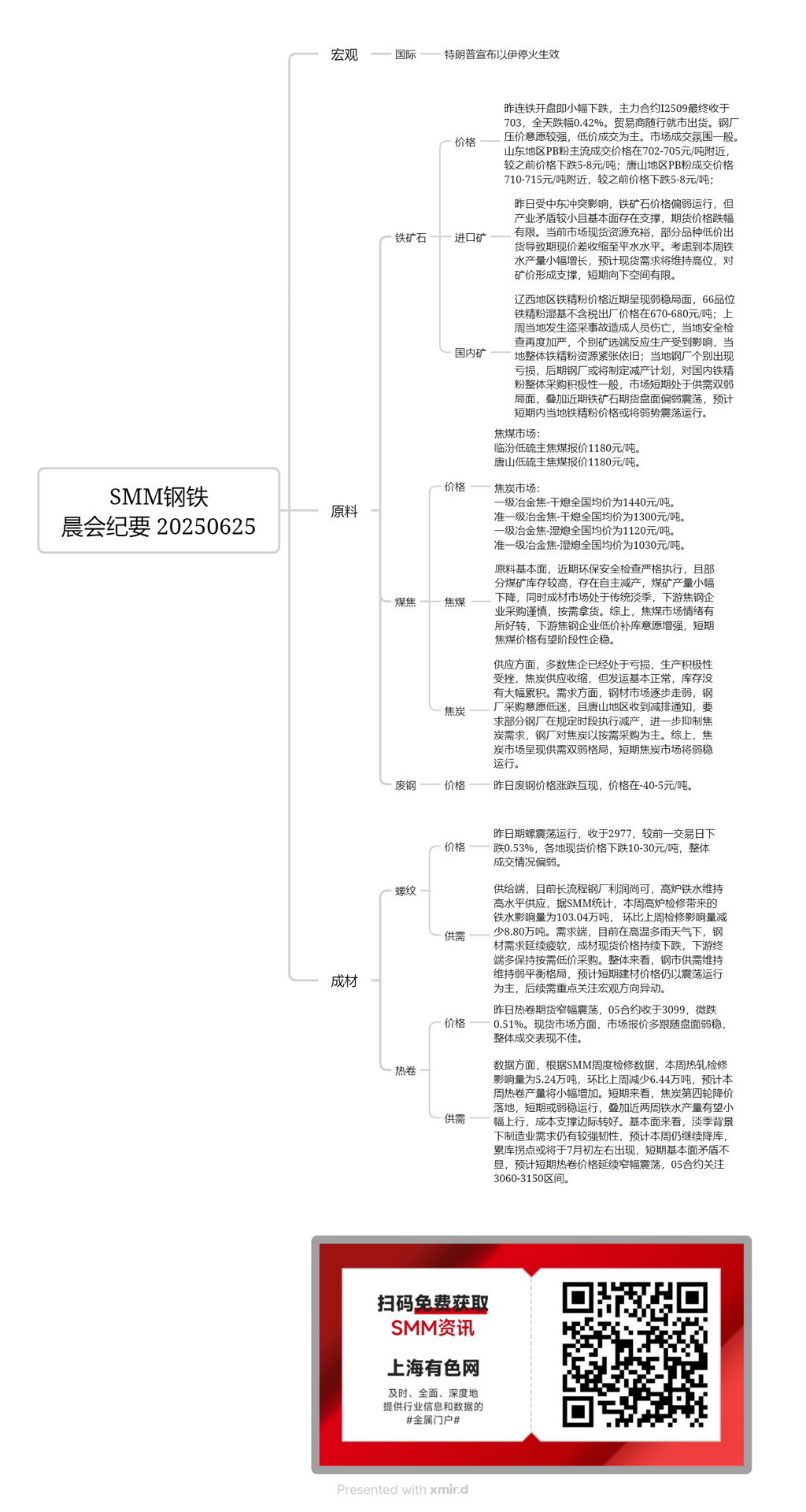

Domestic Ore:

In west Liaoning, the price of iron ore concentrates has been in the doldrums recently. The ex-factory price (excluding tax) of 66% grade iron ore concentrates on a wet basis is 670-680 yuan/mt. Last week, an illegal mining accident occurred in the region, resulting in casualties. As a result, local safety inspections have been tightened again. Some mines and beneficiation plants reported that their production has been affected, and the overall supply of iron ore concentrates in the region remains tight. Some local steel mills are experiencing losses, and they may formulate production cut plans in the future. Their overall enthusiasm for purchasing domestic iron ore concentrates is moderate. The market is currently in a situation of weak supply and demand in the short term. Coupled with the recent weak and volatile performance of the iron ore futures market, it is expected that the price of local iron ore concentrates will remain in the doldrums in the short term.

Imported Ore:

Yesterday, the DCE iron ore futures opened with a slight drop, with the most-traded contract I2509 closing at 703, down 0.42% for the day. Traders sold goods according to market conditions. Steel mills had a strong desire to bargain down prices, and transactions were mainly concluded at lower prices. The market trading atmosphere was moderate. In the Shandong region, the mainstream transaction prices of PB fines were around 702-705 yuan/mt, down 5-8 yuan/mt from previous prices. In the Tangshan region, the transaction prices of PB fines were around 710-715 yuan/mt, also down 5-8 yuan/mt from previous prices. Affected by the Middle East conflict yesterday, iron ore prices were in the doldrums. However, due to relatively small industry contradictions and fundamental support, the decline in futures prices was limited. Currently, spot cargo resources in the market are abundant, and the sale of some varieties at lower prices has led to the spread between futures and spot prices contracting to parity. Considering the slight increase in pig iron production this week, it is expected that spot demand will remain high, providing support for ore prices, with limited downward space in the short term.

Coking Coal:

The quoted price of low-sulphur coking coal in Linfen is 1,180 yuan/mt. The quoted price of low-sulphur coking coal in Tangshan is also 1,180 yuan/mt. Regarding the raw material fundamentals, environmental protection and safety inspections have been strictly enforced recently. Additionally, some coal mines have high inventory levels and have voluntarily cut production, leading to a slight decrease in coal mine production. Meanwhile, the finished steel market is in the traditional off-season, and downstream coking and steel enterprises are cautious in purchasing and purchase as needed. In summary, market sentiment in the coking coal market has improved somewhat. Downstream coking and steel enterprises have increased their willingness to restock at lower prices, and coking coal prices are expected to stabilize in the short term.

Coke:

The nationwide average price of premium metallurgical coke (dry quenching) is 1,440 yuan/mt. The nationwide average price of high-grade metallurgical coke (dry quenching) is 1,300 yuan/mt. The nationwide average price of premium metallurgical coke (wet quenching) is 1,120 yuan/mt. The nationwide average price of high-grade metallurgical coke (wet quenching) is 1,030 yuan/mt. In terms of supply, most coking enterprises are already operating at a loss, and their production enthusiasm has been dampened, leading to a contraction in coke supply. However, shipments are basically normal, and inventory has not accumulated significantly. In terms of demand, the steel market is gradually weakening, and steel mills have low purchase willingness. Moreover, the Tangshan region has received emission reduction notices, requiring some steel mills to implement production cuts during specified periods, further suppressing coke demand. Steel mills mainly purchase coke as needed. In summary, the coke market is experiencing a weak supply and demand scenario, and is expected to remain in the doldrums in the short term.

Rebar:

Yesterday, rebar futures fluctuated rangebound, closing at 2977, down 0.53% from the previous trading day. Spot prices across regions fell by 10-30 yuan/mt, with overall trading activity remaining weak. On the supply side, currently, blast furnace steel mill profits are moderate, and blast furnace pig iron production remains at a high level. According to SMM statistics, the impact of blast furnace maintenance on pig iron production this week was 1.0304 million mt, a decrease of 88,000 mt WoW from the impact of maintenance last week. On the demand side, amidst hot and rainy weather, steel demand continues to be sluggish, with finished steel spot prices continuing to fall. Downstream terminals are mostly purchasing on a need-based basis at low prices. Overall, the steel market maintains a weak balance in supply and demand, and it is expected that short-term construction material prices will continue to fluctuate rangebound, with subsequent focus on macroeconomic direction changes.

HRC:

Yesterday, HRC futures fluctuated rangebound, with the 05 contract closing at 3099, down slightly by 0.51%. In the spot market, market quotes mostly followed the weak and stable trend of the futures market, with overall trading performance being poor. In terms of data, according to SMM's weekly maintenance data, the impact of hot-rolled maintenance this week was 52,400 mt, a decrease of 64,400 mt WoW. It is expected that HRC production will increase slightly this week. In the short term, with the implementation of the fourth round of coke price reductions, coke prices are expected to remain in the doldrums in the short term. Coupled with the expectation of a slight increase in pig iron production over the next two weeks, cost support is expected to improve marginally. From a fundamental perspective, against the backdrop of the off-season, manufacturing demand still shows strong resilience. It is expected that inventory de-stocking will continue this week, with the inventory buildup turning point likely to occur around early July. In the short term, fundamental contradictions are not prominent, and it is expected that HRC prices will continue to fluctuate rangebound, with the 05 contract focusing on the 3060-3150 range.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)